quantlite 0.9.0__tar.gz → 1.0.0__tar.gz

This diff represents the content of publicly available package versions that have been released to one of the supported registries. The information contained in this diff is provided for informational purposes only and reflects changes between package versions as they appear in their respective public registries.

- {quantlite-0.9.0/src/quantlite.egg-info → quantlite-1.0.0}/PKG-INFO +57 -1

- {quantlite-0.9.0 → quantlite-1.0.0}/README.md +56 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/pyproject.toml +1 -1

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/__init__.py +17 -1

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/antifragile/__init__.py +42 -22

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/ergodicity/__init__.py +30 -16

- quantlite-1.0.0/src/quantlite/pipeline.py +338 -0

- quantlite-1.0.0/src/quantlite/regime_integration/__init__.py +31 -0

- quantlite-1.0.0/src/quantlite/regime_integration/portfolio.py +267 -0

- quantlite-1.0.0/src/quantlite/regime_integration/reporting.py +204 -0

- quantlite-1.0.0/src/quantlite/regime_integration/risk.py +212 -0

- {quantlite-0.9.0 → quantlite-1.0.0/src/quantlite.egg-info}/PKG-INFO +57 -1

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite.egg-info/SOURCES.txt +7 -0

- quantlite-1.0.0/tests/test_pipeline.py +165 -0

- quantlite-1.0.0/tests/test_regime_integration.py +287 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/LICENSE +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/setup.cfg +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/backtesting/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/backtesting/analysis.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/backtesting/engine.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/backtesting/legacy.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/backtesting/signals.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/contagion/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/core/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/core/types.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/crypto/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/crypto/exchange.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/crypto/onchain.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/crypto/stablecoin.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/base.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/cache.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/crypto.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/fred.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/local.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/registry.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data/yahoo.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/data_generation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/dependency/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/dependency/clustering.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/dependency/copulas.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/dependency/correlation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/distributions/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/distributions/fat_tails.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/diversification/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/factors/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/factors/classical.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/factors/custom.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/factors/tail_risk.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/forensics/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/instruments/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/instruments/bond_pricing.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/instruments/exotic_options.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/instruments/option_pricing.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/metrics.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/monte_carlo.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/network/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/overfit/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/portfolio/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/portfolio/optimisation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/portfolio/rebalancing.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/regimes/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/regimes/changepoint.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/regimes/conditional.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/regimes/hmm.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/report/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/report/html_renderer.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/report/pdf_renderer.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/report/sections.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/report/tearsheet.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/resample/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/risk/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/risk/evt.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/risk/metrics.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/scenarios/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/simulation/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/simulation/copula_mc.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/simulation/evt_simulation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/simulation/regime_mc.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/visualisation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/dependency.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/plotly_backend/__init__.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/plotly_backend/dependency.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/plotly_backend/portfolio.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/plotly_backend/regimes.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/plotly_backend/risk.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/plotly_backend/theme.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/portfolio.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/regimes.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/risk.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite/viz/theme.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite.egg-info/dependency_links.txt +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite.egg-info/requires.txt +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/src/quantlite.egg-info/top_level.txt +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_analysis.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_antifragile.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_backtesting.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_changepoint.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_clustering.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_conditional.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_contagion.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_copulas.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_correlation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_crypto_exchange.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_crypto_onchain.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_crypto_stablecoin.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_data_connectors.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_data_generation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_diversification.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_engine.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_ergodicity.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_evt.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_factors_classical.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_factors_custom.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_factors_tail_risk.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_fat_tails.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_forensics.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_hmm.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_instruments.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_metrics.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_monte_carlo.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_network.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_optimisation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_overfit.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_plotly_viz.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_rebalancing.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_report.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_resample.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_risk_metrics.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_scenarios.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_signals.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_sim_copula.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_sim_evt.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_sim_regime.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_visualisation.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_viz.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_viz_dependency.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_viz_portfolio.py +0 -0

- {quantlite-0.9.0 → quantlite-1.0.0}/tests/test_viz_regimes.py +0 -0

|

@@ -1,6 +1,6 @@

|

|

|

1

1

|

Metadata-Version: 2.4

|

|

2

2

|

Name: quantlite

|

|

3

|

-

Version: 0.

|

|

3

|

+

Version: 1.0.0

|

|

4

4

|

Summary: A fat-tail-native quantitative finance toolkit: EVT, risk metrics, and honest modelling for markets that bite.

|

|

5

5

|

Author-email: Prasant Sudhakaran <code@prasant.net>

|

|

6

6

|

License: MIT License

|

|

@@ -1096,6 +1096,62 @@ print(f"Tail diversification: {td['tail_diversification']:.3f}")

|

|

|

1096

1096

|

| `quantlite.network` | Correlation networks, eigenvector centrality, cascade simulation, community detection |

|

|

1097

1097

|

| `quantlite.diversification` | Effective Number of Bets, entropy diversification, tail diversification, diversification ratio, Herfindahl index |

|

|

1098

1098

|

|

|

1099

|

+

## v1.0: The Dream API

|

|

1100

|

+

|

|

1101

|

+

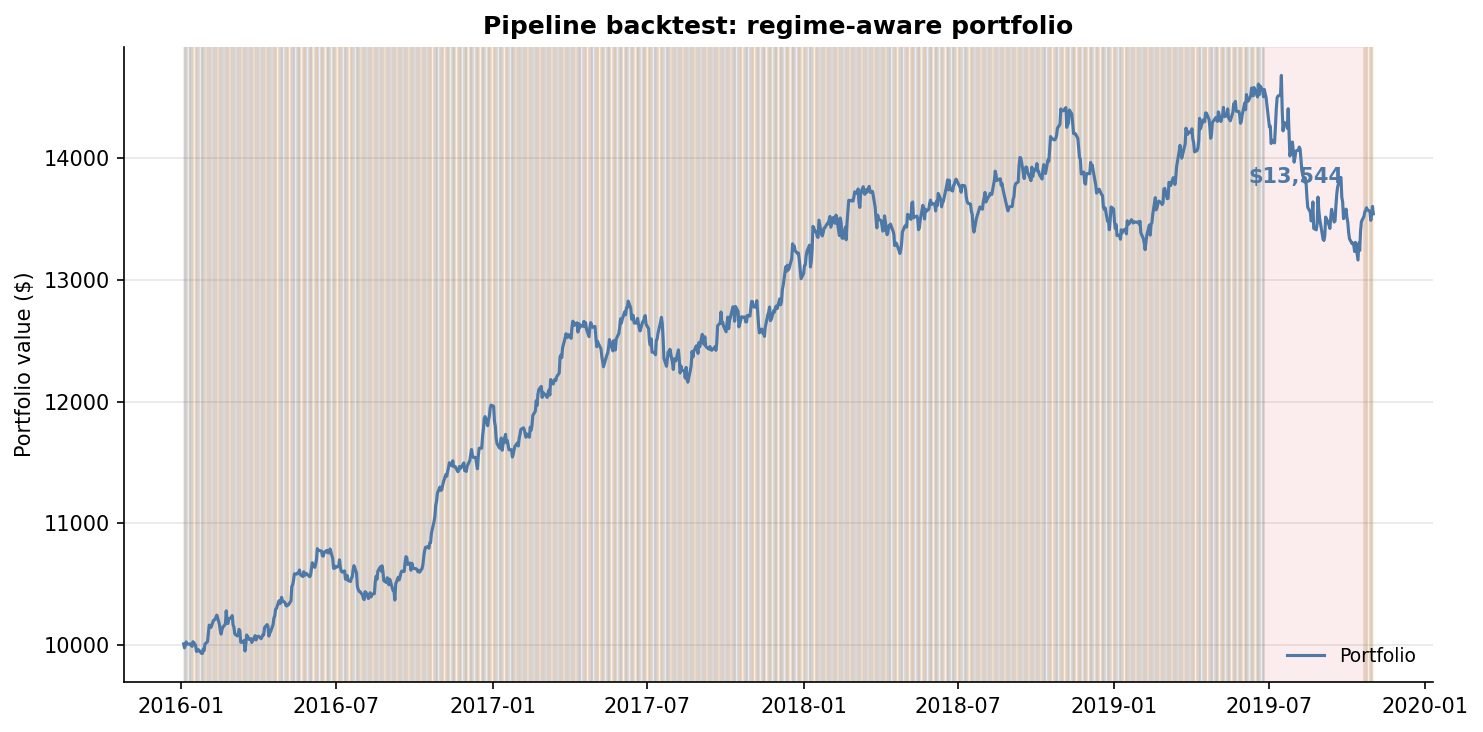

QuantLite v1.0 introduces the **Dream API**, a five-function pipeline that chains the entire quant workflow:

|

|

1102

|

+

|

|

1103

|

+

```python

|

|

1104

|

+

import quantlite as ql

|

|

1105

|

+

|

|

1106

|

+

data = ql.fetch(["AAPL", "BTC-USD", "GLD", "TLT"], period="5y")

|

|

1107

|

+

regimes = ql.detect_regimes(data, n_regimes=3)

|

|

1108

|

+

weights = ql.construct_portfolio(data, regime_aware=True, regimes=regimes)

|

|

1109

|

+

result = ql.backtest(data, weights)

|

|

1110

|

+

ql.tearsheet(result, regimes=regimes, save="portfolio.txt")

|

|

1111

|

+

```

|

|

1112

|

+

|

|

1113

|

+

### Regime-Aware Portfolio Construction

|

|

1114

|

+

|

|

1115

|

+

Weights automatically tilt defensive during crisis regimes, increasing allocations to bonds and gold while reducing equity exposure:

|

|

1116

|

+

|

|

1117

|

+

|

|

1118

|

+

|

|

1119

|

+

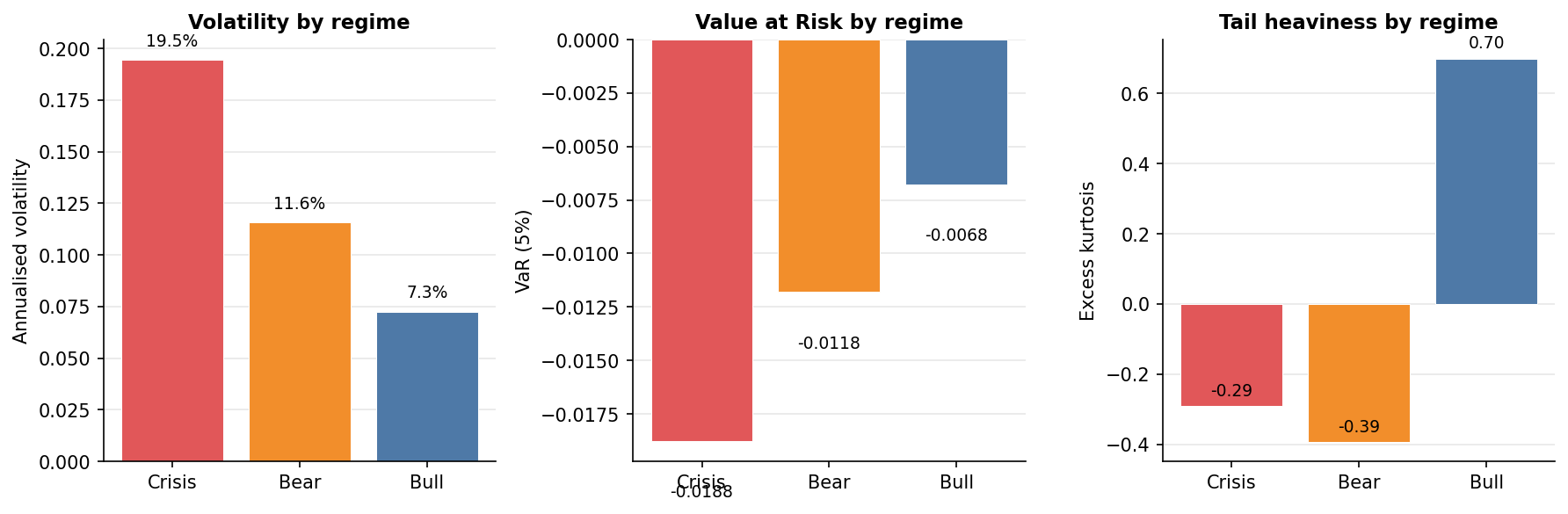

### Regime Risk Analysis

|

|

1120

|

+

|

|

1121

|

+

VaR, CVaR, volatility, skewness, and kurtosis computed separately for each market regime:

|

|

1122

|

+

|

|

1123

|

+

|

|

1124

|

+

|

|

1125

|

+

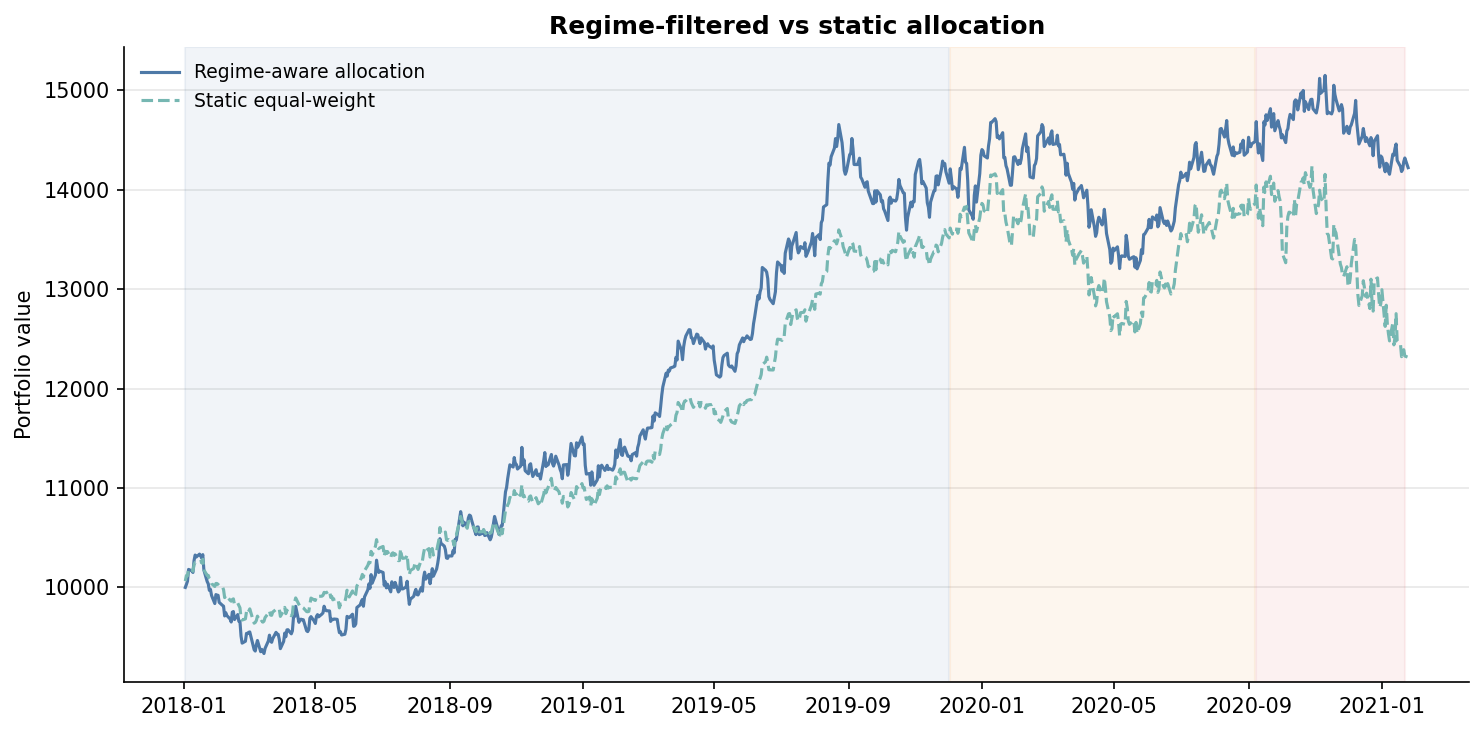

### Regime-Filtered Backtesting

|

|

1126

|

+

|

|

1127

|

+

Different weight sets applied per regime, with full performance attribution:

|

|

1128

|

+

|

|

1129

|

+

|

|

1130

|

+

|

|

1131

|

+

### v1.0 Module Reference

|

|

1132

|

+

|

|

1133

|

+

| Module | Description |

|

|

1134

|

+

|--------|-------------|

|

|

1135

|

+

| `quantlite.pipeline` | Dream API: `fetch`, `detect_regimes`, `construct_portfolio`, `backtest`, `tearsheet` |

|

|

1136

|

+

| `quantlite.regime_integration` | Regime-conditional risk, defensive portfolio tilting, filtered backtesting, tearsheets |

|

|

1137

|

+

| `quantlite.regimes` | HMM regime detection, Bayesian changepoint detection, conditional metrics |

|

|

1138

|

+

| `quantlite.portfolio` | Markowitz, CVaR, risk parity, HRP, Black-Litterman, Kelly optimisation |

|

|

1139

|

+

| `quantlite.backtesting` | Multi-asset engine with circuit breakers, slippage, regime-aware signals |

|

|

1140

|

+

| `quantlite.risk` | VaR, CVaR, Sortino, Calmar, omega ratio, tail ratio, drawdown analysis |

|

|

1141

|

+

| `quantlite.data` | Unified fetching: Yahoo Finance, CCXT, FRED, local files |

|

|

1142

|

+

| `quantlite.distributions` | Student-t, stable, GPD, GEV fitting and simulation |

|

|

1143

|

+

| `quantlite.simulation` | Fat-tail Monte Carlo: EVT-based, copula-based engines |

|

|

1144

|

+

| `quantlite.viz` | Stephen Few-inspired charts: regimes, portfolios, risk dashboards |

|

|

1145

|

+

| `quantlite.factors` | Classical factors, custom factors, tail risk factors |

|

|

1146

|

+

| `quantlite.ergodicity` | Time-average vs ensemble-average growth, Kelly sizing |

|

|

1147

|

+

| `quantlite.antifragile` | Barbell metrics, convexity scores, stress testing |

|

|

1148

|

+

| `quantlite.scenarios` | Historical, hypothetical, and Monte Carlo scenario analysis |

|

|

1149

|

+

| `quantlite.forensics` | Overfitting detection, data snooping tests, walk-forward analysis |

|

|

1150

|

+

| `quantlite.contagion` | CoVaR, Delta CoVaR, MES, Granger causality |

|

|

1151

|

+

| `quantlite.network` | Correlation networks, centrality, cascade simulation |

|

|

1152

|

+

| `quantlite.diversification` | Effective Number of Bets, entropy, tail diversification |

|

|

1153

|

+

| `quantlite.crypto` | On-chain risk, stablecoin depeg, exchange risk scoring |

|

|

1154

|

+

|

|

1099

1155

|

## Design Philosophy

|

|

1100

1156

|

|

|

1101

1157

|

1. **Fat tails are the default.** Gaussian assumptions are explicitly opt-in, never implicit.

|

|

@@ -1015,6 +1015,62 @@ print(f"Tail diversification: {td['tail_diversification']:.3f}")

|

|

|

1015

1015

|

| `quantlite.network` | Correlation networks, eigenvector centrality, cascade simulation, community detection |

|

|

1016

1016

|

| `quantlite.diversification` | Effective Number of Bets, entropy diversification, tail diversification, diversification ratio, Herfindahl index |

|

|

1017

1017

|

|

|

1018

|

+

## v1.0: The Dream API

|

|

1019

|

+

|

|

1020

|

+

QuantLite v1.0 introduces the **Dream API**, a five-function pipeline that chains the entire quant workflow:

|

|

1021

|

+

|

|

1022

|

+

```python

|

|

1023

|

+

import quantlite as ql

|

|

1024

|

+

|

|

1025

|

+

data = ql.fetch(["AAPL", "BTC-USD", "GLD", "TLT"], period="5y")

|

|

1026

|

+

regimes = ql.detect_regimes(data, n_regimes=3)

|

|

1027

|

+

weights = ql.construct_portfolio(data, regime_aware=True, regimes=regimes)

|

|

1028

|

+

result = ql.backtest(data, weights)

|

|

1029

|

+

ql.tearsheet(result, regimes=regimes, save="portfolio.txt")

|

|

1030

|

+

```

|

|

1031

|

+

|

|

1032

|

+

### Regime-Aware Portfolio Construction

|

|

1033

|

+

|

|

1034

|

+

Weights automatically tilt defensive during crisis regimes, increasing allocations to bonds and gold while reducing equity exposure:

|

|

1035

|

+

|

|

1036

|

+

|

|

1037

|

+

|

|

1038

|

+

### Regime Risk Analysis

|

|

1039

|

+

|

|

1040

|

+

VaR, CVaR, volatility, skewness, and kurtosis computed separately for each market regime:

|

|

1041

|

+

|

|

1042

|

+

|

|

1043

|

+

|

|

1044

|

+

### Regime-Filtered Backtesting

|

|

1045

|

+

|

|

1046

|

+

Different weight sets applied per regime, with full performance attribution:

|

|

1047

|

+

|

|

1048

|

+

|

|

1049

|

+

|

|

1050

|

+

### v1.0 Module Reference

|

|

1051

|

+

|

|

1052

|

+

| Module | Description |

|

|

1053

|

+

|--------|-------------|

|

|

1054

|

+

| `quantlite.pipeline` | Dream API: `fetch`, `detect_regimes`, `construct_portfolio`, `backtest`, `tearsheet` |

|

|

1055

|

+

| `quantlite.regime_integration` | Regime-conditional risk, defensive portfolio tilting, filtered backtesting, tearsheets |

|

|

1056

|

+

| `quantlite.regimes` | HMM regime detection, Bayesian changepoint detection, conditional metrics |

|

|

1057

|

+

| `quantlite.portfolio` | Markowitz, CVaR, risk parity, HRP, Black-Litterman, Kelly optimisation |

|

|

1058

|

+

| `quantlite.backtesting` | Multi-asset engine with circuit breakers, slippage, regime-aware signals |

|

|

1059

|

+

| `quantlite.risk` | VaR, CVaR, Sortino, Calmar, omega ratio, tail ratio, drawdown analysis |

|

|

1060

|

+

| `quantlite.data` | Unified fetching: Yahoo Finance, CCXT, FRED, local files |

|

|

1061

|

+

| `quantlite.distributions` | Student-t, stable, GPD, GEV fitting and simulation |

|

|

1062

|

+

| `quantlite.simulation` | Fat-tail Monte Carlo: EVT-based, copula-based engines |

|

|

1063

|

+

| `quantlite.viz` | Stephen Few-inspired charts: regimes, portfolios, risk dashboards |

|

|

1064

|

+

| `quantlite.factors` | Classical factors, custom factors, tail risk factors |

|

|

1065

|

+

| `quantlite.ergodicity` | Time-average vs ensemble-average growth, Kelly sizing |

|

|

1066

|

+

| `quantlite.antifragile` | Barbell metrics, convexity scores, stress testing |

|

|

1067

|

+

| `quantlite.scenarios` | Historical, hypothetical, and Monte Carlo scenario analysis |

|

|

1068

|

+

| `quantlite.forensics` | Overfitting detection, data snooping tests, walk-forward analysis |

|

|

1069

|

+

| `quantlite.contagion` | CoVaR, Delta CoVaR, MES, Granger causality |

|

|

1070

|

+

| `quantlite.network` | Correlation networks, centrality, cascade simulation |

|

|

1071

|

+

| `quantlite.diversification` | Effective Number of Bets, entropy, tail diversification |

|

|

1072

|

+

| `quantlite.crypto` | On-chain risk, stablecoin depeg, exchange risk scoring |

|

|

1073

|

+

|

|

1018

1074

|

## Design Philosophy

|

|

1019

1075

|

|

|

1020

1076

|

1. **Fat tails are the default.** Gaussian assumptions are explicitly opt-in, never implicit.

|

|

@@ -4,7 +4,7 @@ build-backend = "setuptools.build_meta"

|

|

|

4

4

|

|

|

5

5

|

[project]

|

|

6

6

|

name = "quantlite"

|

|

7

|

-

version = "0.

|

|

7

|

+

version = "1.0.0"

|

|

8

8

|

description = "A fat-tail-native quantitative finance toolkit: EVT, risk metrics, and honest modelling for markets that bite."

|

|

9

9

|

requires-python = ">=3.9"

|

|

10

10

|

license = { file = "LICENSE" }

|

|

@@ -6,7 +6,7 @@ portfolio optimisation, multi-asset backtesting, and

|

|

|

6

6

|

Stephen Few-inspired visualisation.

|

|

7

7

|

"""

|

|

8

8

|

|

|

9

|

-

__version__ = "0.

|

|

9

|

+

__version__ = "1.0.0"

|

|

10

10

|

|

|

11

11

|

from .backtesting import (

|

|

12

12

|

BacktestConfig,

|

|

@@ -79,6 +79,14 @@ __all__ = [

|

|

|

79

79

|

"crypto",

|

|

80

80

|

# Fat-tail Monte Carlo simulation

|

|

81

81

|

"simulation",

|

|

82

|

+

# Regime-aware integration

|

|

83

|

+

"regime_integration",

|

|

84

|

+

# Dream API (pipeline)

|

|

85

|

+

"fetch",

|

|

86

|

+

"detect_regimes",

|

|

87

|

+

"construct_portfolio",

|

|

88

|

+

"backtest",

|

|

89

|

+

"tearsheet",

|

|

82

90

|

]

|

|

83

91

|

|

|

84

92

|

from . import ( # noqa: E402

|

|

@@ -90,7 +98,15 @@ from . import ( # noqa: E402

|

|

|

90

98

|

forensics,

|

|

91

99

|

network,

|

|

92

100

|

overfit,

|

|

101

|

+

regime_integration,

|

|

93

102

|

resample,

|

|

94

103

|

scenarios,

|

|

95

104

|

simulation,

|

|

96

105

|

)

|

|

106

|

+

from .pipeline import ( # noqa: E402

|

|

107

|

+

backtest,

|

|

108

|

+

construct_portfolio,

|

|

109

|

+

detect_regimes,

|

|

110

|

+

tearsheet,

|

|

111

|

+

)

|

|

112

|

+

from .pipeline import fetch as fetch # noqa: E402

|

|

@@ -218,44 +218,40 @@ def barbell_allocation(

|

|

|

218

218

|

def lindy_estimate(age: float, confidence: float = 0.95) -> dict[str, float]:

|

|

219

219

|

"""Estimate remaining life expectancy using the Lindy effect.

|

|

220

220

|

|

|

221

|

-

|

|

222

|

-

|

|

221

|

+

Models non-perishable entities (ideas, technologies, institutions)

|

|

222

|

+

with a Pareto survival distribution (alpha = 1). Under this model:

|

|

223

223

|

|

|

224

|

-

|

|

225

|

-

|

|

224

|

+

P(T > age + t | T > age) = age / (age + t)

|

|

225

|

+

|

|

226

|

+

Key properties:

|

|

227

|

+

|

|

228

|

+

* **Expected remaining life** = age (the longer it has survived,

|

|

229

|

+

the longer we expect it to last).

|

|

230

|

+

* **Lower bound at confidence level c**: the additional time *t*

|

|

231

|

+

such that we are *c*-confident the entity survives at least *t*

|

|

232

|

+

more units. Solve ``age / (age + t) = 1 - c`` to get

|

|

233

|

+

``t = age * c / (1 - c)``.

|

|

226

234

|

|

|

227

235

|

Parameters

|

|

228

236

|

----------

|

|

229

237

|

age : float

|

|

230

238

|

Current age of the entity (in any consistent unit).

|

|

231

239

|

confidence : float

|

|

232

|

-

Confidence level for the survival bound (default 0.95).

|

|

240

|

+

Confidence level for the survival lower bound (default 0.95).

|

|

233

241

|

|

|

234

242

|

Returns

|

|

235

243

|

-------

|

|

236

244

|

dict

|

|

237

|

-

Keys: 'age', 'expected_remaining' (

|

|

238

|

-

|

|

245

|

+

Keys: 'age', 'expected_remaining', 'lower_bound' (at the

|

|

246

|

+

given confidence), 'total_expected'.

|

|

239

247

|

"""

|

|

240

248

|

if age <= 0:

|

|

241

249

|

raise ValueError("age must be positive")

|

|

242

250

|

if not 0 < confidence < 1:

|

|

243

251

|

raise ValueError("confidence must be between 0 and 1")

|

|

244

252

|

|

|

245

|

-

# Under Lindy (Pareto with alpha=1), expected remaining life = age

|

|

246

253

|

expected_remaining = age

|

|

247

|

-

|

|

248

|

-

# Lower bound: at confidence level, survival beyond this point

|

|

249

|

-

# P(survive t more) = age / (age + t), so t = age * (1/p - 1)

|

|

250

|

-

lower_bound = age * (1.0 / (1.0 - confidence) - 1.0) * (1.0 - confidence)

|

|

251

|

-

# Simplifies to: age * confidence / (1 - confidence) * (1 - confidence) = age * confidence

|

|

252

|

-

# Actually: P(T > age + t | T > age) = age / (age + t) for Pareto

|

|

253

|

-

# Set this = 1 - confidence: age/(age+t) = 1 - confidence

|

|

254

|

-

# t = age * confidence / (1 - confidence)

|

|

255

|

-

lower_bound = age * (1.0 - confidence) / confidence

|

|

256

|

-

# That's the point we're confident we'll reach (small value)

|

|

257

|

-

# More useful: expected remaining at median

|

|

258

|

-

# P(T > age + t | T > age) = 0.5 => t = age (median remaining = age)

|

|

254

|

+

lower_bound = age * confidence / (1.0 - confidence)

|

|

259

255

|

|

|

260

256

|

return {

|

|

261

257

|

"age": age,

|

|

@@ -268,11 +264,25 @@ def lindy_estimate(age: float, confidence: float = 0.95) -> dict[str, float]:

|

|

|

268

264

|

def skin_in_game_score(

|

|

269

265

|

manager_returns: ArrayLike,

|

|

270

266

|

fund_returns: ArrayLike,

|

|

267

|

+

alignment_weight: float = 0.4,

|

|

268

|

+

downside_weight: float = 0.4,

|

|

269

|

+

asymmetry_weight: float = 0.2,

|

|

271

270

|

) -> dict[str, float]:

|

|

272

271

|

"""Measure principal-agent alignment via payoff asymmetry.

|

|

273

272

|

|

|

274

273

|

Compares the manager's exposure to downside vs upside relative

|

|

275

|

-

to the fund.

|

|

274

|

+

to the fund. A good score means the manager shares the pain.

|

|

275

|

+

|

|

276

|

+

The composite score weights three components:

|

|

277

|

+

|

|

278

|

+

* **Alignment** (default 0.4): correlation between manager and fund

|

|

279

|

+

returns. Are incentives actually correlated?

|

|

280

|

+

* **Downside sharing** (default 0.4): when the fund loses, does the

|

|

281

|

+

manager bleed proportionally? This matters as much as alignment —

|

|

282

|

+

asymmetric downside is the hallmark of agency problems.

|

|

283

|

+

* **Upside asymmetry** (default 0.2): does the manager capture

|

|

284

|

+

disproportionate upside? A secondary check — some asymmetry is

|

|

285

|

+

expected (performance fees), but extreme values signal misalignment.

|

|

276

286

|

|

|

277

287

|

Parameters

|

|

278

288

|

----------

|

|

@@ -280,6 +290,12 @@ def skin_in_game_score(

|

|

|

280

290

|

Returns experienced by the manager (compensation-adjusted).

|

|

281

291

|

fund_returns : array-like

|

|

282

292

|

Returns experienced by the fund investors.

|

|

293

|

+

alignment_weight : float

|

|

294

|

+

Weight for the alignment (correlation) component (default 0.4).

|

|

295

|

+

downside_weight : float

|

|

296

|

+

Weight for the downside-sharing component (default 0.4).

|

|

297

|

+

asymmetry_weight : float

|

|

298

|

+

Weight for the upside-asymmetry component (default 0.2).

|

|

283

299

|

|

|

284

300

|

Returns

|

|

285

301

|

-------

|

|

@@ -317,7 +333,11 @@ def skin_in_game_score(

|

|

|

317

333

|

|

|

318

334

|

# Composite score: high alignment + high downside sharing + low upside asymmetry = good

|

|

319

335

|

# Normalise to [0, 1] approximately

|

|

320

|

-

score = (

|

|

336

|

+

score = (

|

|

337

|

+

alignment * alignment_weight

|

|

338

|

+

+ min(downside_sharing, 1.0) * downside_weight

|

|

339

|

+

+ max(0, 1.0 - abs(upside_asymmetry - 1.0)) * asymmetry_weight

|

|

340

|

+

)

|

|

321

341

|

|

|

322

342

|

return {

|

|

323

343

|

"alignment": alignment,

|

|

@@ -91,11 +91,13 @@ def ergodicity_gap(returns: ArrayLike) -> float:

|

|

|

91

91

|

def kelly_fraction(returns: ArrayLike, risk_free: float = 0.0) -> float:

|

|

92

92

|

"""Compute the optimal Kelly fraction for geometric growth.

|

|

93

93

|

|

|

94

|

-

The Kelly criterion maximises the expected logarithmic growth rate

|

|

95

|

-

For a simple binary-style approximation from empirical returns,

|

|

96

|

-

we optimise f to maximise E[log(1 + f * (r - risk_free))].

|

|

94

|

+

The Kelly criterion maximises the expected logarithmic growth rate:

|

|

97

95

|

|

|

98

|

-

|

|

96

|

+

f* = argmax_f E[log(1 + f * (r - r_f))]

|

|

97

|

+

|

|

98

|

+

Uses ``scipy.optimize.minimize_scalar`` with bounded search on

|

|

99

|

+

[-0.5, 3.0]. Falls back to Brent-bounded optimisation if the

|

|

100

|

+

primary solve fails.

|

|

99

101

|

|

|

100

102

|

Parameters

|

|

101

103

|

----------

|

|

@@ -110,24 +112,36 @@ def kelly_fraction(returns: ArrayLike, risk_free: float = 0.0) -> float:

|

|

|

110

112

|

Optimal fraction of capital to deploy. Can be < 0 (short)

|

|

111

113

|

or > 1 (leveraged).

|

|

112

114

|

"""

|

|

115

|

+

from scipy.optimize import minimize_scalar

|

|

116

|

+

|

|

113

117

|

r = _to_array(returns)

|

|

114

118

|

excess = r - risk_free

|

|

115

119

|

|

|

116

|

-

|

|

117

|

-

fractions = np.linspace(-0.5, 3.0, 3500)

|

|

118

|

-

best_f = 0.0

|

|

119

|

-

best_g = -np.inf

|

|

120

|

-

|

|

121

|

-

for f in fractions:

|

|

120

|

+

def neg_expected_log_growth(f: float) -> float:

|

|

122

121

|

portfolio = 1.0 + f * excess

|

|

123

122

|

if np.any(portfolio <= 0):

|

|

124

|

-

|

|

125

|

-

|

|

126

|

-

|

|

127

|

-

|

|

128

|

-

|

|

123

|

+

return 1e10 # infeasible

|

|

124

|

+

return -float(np.mean(np.log(portfolio)))

|

|

125

|

+

|

|

126

|

+

bounds = (-0.5, 3.0)

|

|

127

|

+

|

|

128

|

+

result = minimize_scalar(

|

|

129

|

+

neg_expected_log_growth, bounds=bounds, method="bounded",

|

|

130

|

+

options={"xatol": 1e-8, "maxiter": 500},

|

|

131

|

+

)

|

|

132

|

+

|

|

133

|

+

if result.success:

|

|

134

|

+

return float(round(result.x, 4))

|

|

135

|

+

|

|

136

|

+

# Fallback: try again with Brent in the same interval

|

|

137

|

+

result2 = minimize_scalar(

|

|

138

|

+

neg_expected_log_growth, bracket=(-0.5, 0.5, 3.0), method="brent",

|

|

139

|

+

)

|

|

140

|

+

if result2.success and bounds[0] <= result2.x <= bounds[1]:

|

|

141

|

+

return float(round(result2.x, 4))

|

|

129

142

|

|

|

130

|

-

return

|

|

143

|

+

# Last resort: return 0 (no bet)

|

|

144

|

+

return 0.0

|

|

131

145

|

|

|

132

146

|

|

|

133

147

|

def leverage_effect(

|